Parag Patadiya

Partner - Head of Assurance Services

Background

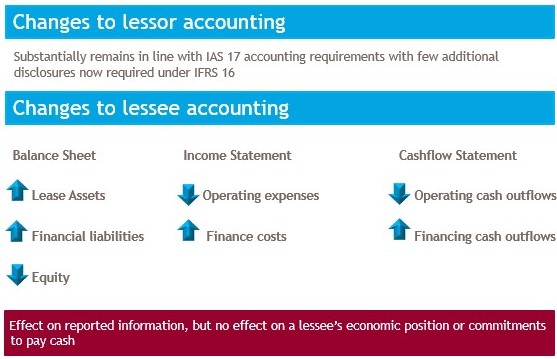

IFRS 16 Leases fundamentally changes the financial reporting landscape for how lessees account for operating leases. The new standard effectively removes the operating leases classification and requires all lessees to show a lease liability and a corresponding right-of-use asset for all leases (with some limited exceptions).

Entities need to ascertain what actions need to be taken so as to allow them to prepare their financial statements using this new accounting standard. The changes can be complex and have effects beyond just the accounting treatment.

As the choices made will affect the way the performance of the business is measured and reported, it is vital to consider not only the commercial and practical issues, but also the tax implications of these changes.

Steps to implementation

Our experts in this area can help you establish the impact of IFRS 16 implementation and advise on what actions you should be taking.

Questions which should be asked for adoption include:

Project management, Board sponsorship and communication with those charged with governance:

Detailed effects:

For more details and guidance on IFRS 16 application, please see IFRS Publications by BDO.