Parag Patadiya

Partner - Head of Assurance Services

Background

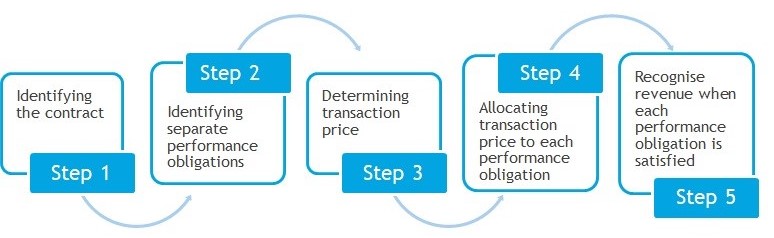

IFRS 15 brings a new and detailed approach to accounting for revenue, and is likely to have far reaching effects across a wide range of industries. It is based around a new ‘5 step’ model and contains a comprehensive set of requirements which are different from the current guidance in IFRS. Some of the differences are more obvious, while others arise from subtle changes in the detail that are not immediately apparent.

While IFRS 15 affects almost all entities in all industry sectors, the most significant changes to date have arisen at larger entities in the telecommunications, software, technology, real estate, pharmaceutical, construction and engineering, aerospace and defence, and automotive sectors. However, this is likely to be because those entities were aware that IFRS 15 would have a significant effect on them and have moved relatively quickly with their implementation projects. Entities in other sectors, and medium sized and smaller entities, are lagging and are running out of time. The adoption of IFRS 15 requires a detailed review to be carried out of all contracts that have been entered into.

The Five Step Model

Our IFRS 15 experts can help you determine the impact of the new standard on your reported earnings.

Questions which should be asked for adoption include:

Project management, Board sponsorship and communication with those charged with governance:

Detailed effects:

For more details and guidance on IFRS 9 application, please see IFRS Publications by BDO.