Background

As per Article 51 of the Federal Decree Law No. 47 of 2022 (‘UAE CT Law’) prescribes that a Taxable Person is required to register[1] for UAE Corporate Tax (‘CT’) within the timeline prescribed by the Federal Tax Authority (‘FTA’). As per an answer provided via FAQ[2] on Ministry of Finance’s (MOF) portal, indicated that all Taxable Persons must be registered prior to filing their first return.

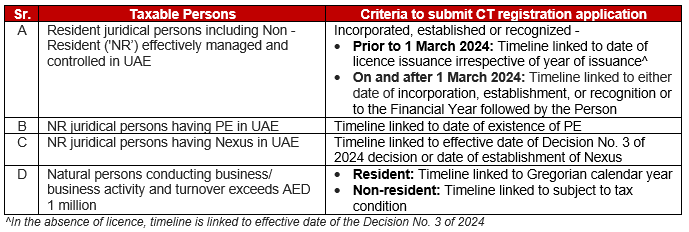

Recent publication on registration timeframe

Recently, the FTA vide its Decision No. 3 of 2024 (effective from 1 March 2024) has prescribed the timelines for submitting UAE CT registration application. All Taxable Persons need to analyse the timeline relevant for them with respect to CT registration based the following criteria:

Penal consequences

One-time penalty of AED 10,000 for delay in submitting CT registration application will be non-deductible for computing the taxable income.

Way forward

It is imperative for businesses to evaluate their CT registration obligation basis the prescribed criteria and due dates attached to such criteria. More importantly, for NR juridical persons and natural persons as the parameters to be evaluated appear to be subjective. Furthermore, as the CT registration is to be submitted on Emara Tax Portal, it is suggested to commence the evaluation at the earliest so that the procedures that needs to be undertaken on such Portal is completed at the earliest to meet the applicable timelines and avoid penal consequences.

How can we help?

Our tax experts can help evaluate businesses having business operations in UAE with determining CT registration due dates and subsequently, assist in making CT registration application and follow-up for obtaining the same

[1] Ministerial Decision No. 43 of 2023 provides exceptions from CT registration for certain Persons

[2] FAQ No. 328 (https://mof.gov.ae/corporate-tax-faq/)